|

Property Search Results

Parcel ID: 500-0920-0012-00 Address: 2678 NEWTOWN RD Index Order: Owner Card: 1 of 1 Tax Dist 042 ANDERSON-FOREST HILLS-00030 School Dist 4 FOREST HILLS LSD Land Use 510 Single family Dwlg Finished Square Ft. 2179 Acres 3.352 Appraisal Area 50058 AND 58 Year Built 1910 Total Rooms 7 # of Bedrooms 4 Full Bathrooms 1 Half Bathrooms 1 |

Board of Revision No Homestead No 2.5% / Stadium Credit Yes Divided Property No New Construction No Foreclosure No Date 12/29/93 Conveyance # 19930 Sale Amount $0 Other Mkt Land Value 153,400 Cauv Value 0 Mkt Impr Value 54,900 Mkt Total Value 208,300 # of Parcels 1 Deed Type 12 Deed Number 1993713738 |

| Along with this picture of the Sayre home enwreathed in summertime and honeysuckle, was a set of three nearby homes, with an assortment of features. They approximated the square footage but the most noticeable similarity was their proximity: each was within a half mile of the Sayre land. Recognizing that the value of the land was the major piece of the assessment process for an older home like the Sayre´s, proximity would be important since nearby homes would have the most similar views and land values. Each of them mentioned "Good Grade" in the description of the land. |

|

|

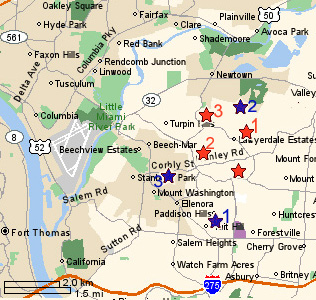

$ 79,000 MLS867985 - view of KY, rolling wooded, private 1.44 Acres, water/sewer at street $105,000 MLS844146 - 400' driveway, 3 Acres, no improvements The Sayres is the unnumbered star |

|

| 7083 Paddison | $200,000 | 2.1 Ac | 53 yo |

| 7114 Ragland | $197,000 | 4.8 Ac | 43 yo |

| 6600 Corbly | $164,000 | 2.3 Ac | 62yo |

|

Appraiser´s doubly penalizing comps (in blue): 7083 Paddison (sold 7/03 for $200,000 with 2.18 ac land $83,000 and avg grade 7114 Ragland (sold 9/02 for $197,000 with 4.85 ac land $103,000 and avg grade 6600 Corbly (sold 6/02 for $164,000 with 2.3 ac land $84,000 and avg grade |

The Sayre home is the unnumbered star. |

Auditor´s Comps (in red): 7452 Heatherwood (sold 7/01 for $229,000 with .54 ac land $63,000 and good grade) 2480 Royalview (sold 5/01 for $215,000 with 1.07 ac land $70,000 and good grade) 6939 Treeridge (sold 4/01 for $267,000 with .67 ac land $85,000 and good grade) |

|---|

|

With an initial cost of $4,200 (to replace furnace-boiler and water heaters in a worst case scenario, less for insulation), an annual implied potential savings of almost $1,250, and an interest rate on liquid savings of 2%, the payback stream is pretty impressive: |

|

| Reproduction cost-new of | improvements [house] | 2179sf @ $75/sf = | $163,425 |

| [garage] | 510sf @ $22/sf = | $ 11,220 | |

| Less depreciation - physical | - $139,716 |

| Home | Selling price | Quality of construction | Condition | Living Area |

| Sayre | "fair" | "fair/poor" | 2179sf | |

|---|---|---|---|---|

| #1. | $200,000 | "avg" -$10,000 | "fair" -$50,000 | 2073sf --- |

| #2. | $197,000 | "avg" -$10,000 | "avg" -$80,000 | 1530sf + $10,000 |

| #3. | $164,000 | "avg" -$10,000 | "avg" -$80,000 | 2623sf -$10,000 |

| Home | House Portion of Selling price | Quality of construction | Condition | Living Area |

| Sayre | "fair" | "fair/poor" | 2179sf | |

|---|---|---|---|---|

| #1. | $105,000 | "avg" -$10,000 | "fair" -$26,000 | 2073sf --- |

| #2. | $ 99,000 | "avg" -$10,000 | "avg" -$49,000 | 1530sf + $18,000 |

| #3. | $ 87,000 | "avg" -$10,000 | "avg" -$43,000 | 2623sf -$18,000 |